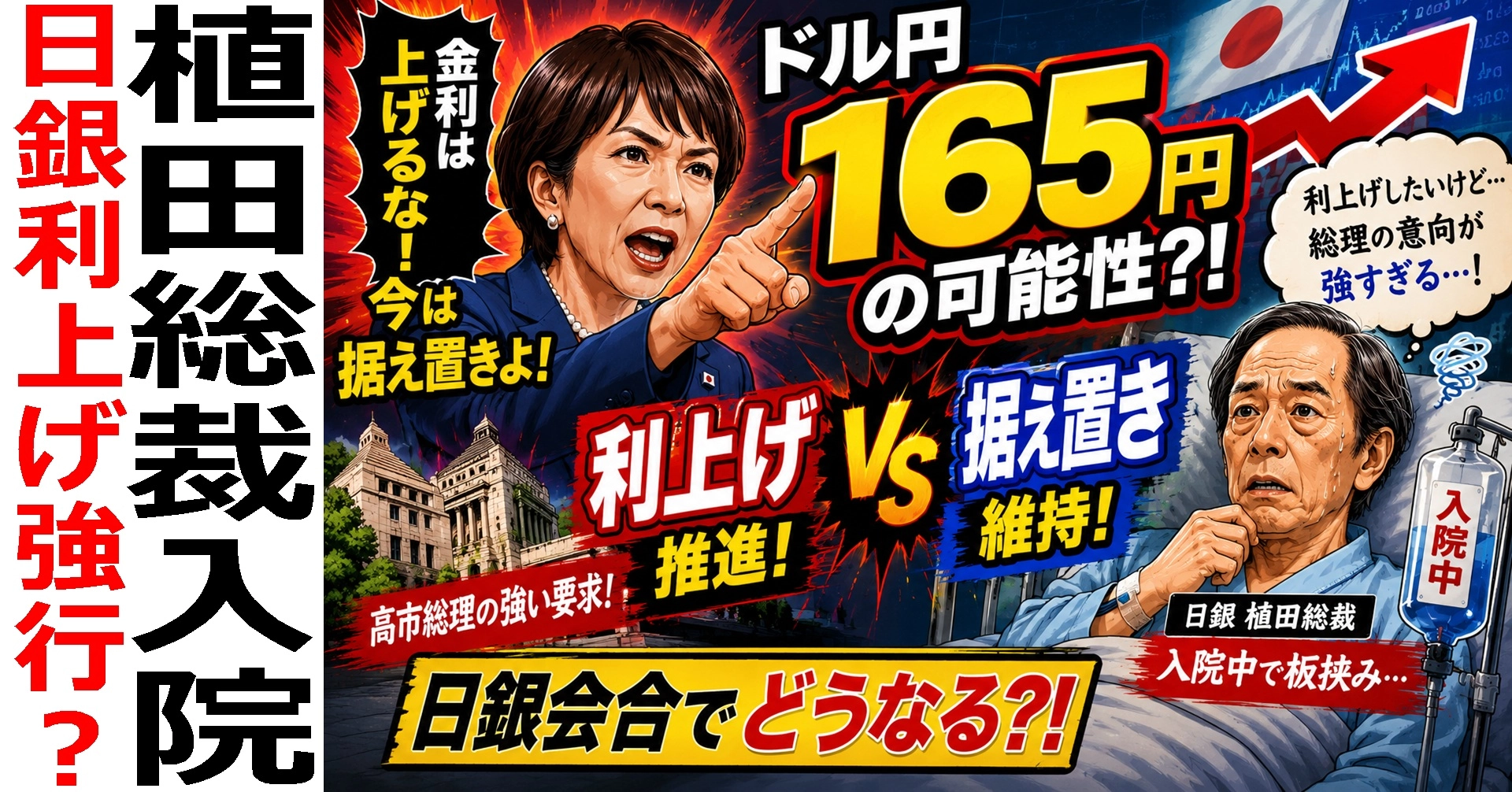

What is the possibility of USD/JPY reaching 165? BoJ rate hike vs. hold—what will happen? The Shadow of the Tachibana Administration and the Ripple of Governor Ueda’s Hospitalization

Everyone, with the dollar/yen stabilizing in the 160 level, many may be wondering “Will there be intervention?” “Will rates rises strengthen the yen?”

In Japan, which is highly dependent on imports, price increases driven by a weaker yen are directly hitting households. Gasoline costs, electricity, and food, essential living items, continue to rise.

As of June 2026, the market remains nervy ahead of strong U.S. employment data, regional tensions in the Middle East, and the Bank of Japan’s Policy Meeting. Additionally, the surprising news of Governor Ueda Kazuo’s hospitalization has been added.

Will the BOJ move to raise rates? And would a rate hike really curb the yen’s depreciation?

This time, we will explain and organize the possibilities of intervention, the June 15–16 BOJ meeting, the impact of Governor Ueda’s hospitalization, and relations with the Takai administration.

?FX New Generation: One-Click FX Training MAX

?160 Yen Trend Stabilized! The Psychological Intervention Line Fear

The current USD/JPY is hovering in the low 160s, with the 160s having become a stable level in the market.

There is no clear turning point in the currency market, but the 160 level holds special meaning for market participants. Because the government and BOJ have shown strong vigilance in the past, it is regarded as an “intervention alert line.”

However, the characteristic this time is that the rise is relatively gradual rather than sharp.

What markets are most wary of is rapid fluctuations. A gradual yen depreciation is less noticeable, but the burden on importing companies and ordinary households is certainly increasing.

It can be said that the situation is precisely “inflation driven by a weaker yen.”

?Will there be intervention? No? The Finance Ministry’s empty rhetoric and past performance

Many people are concerned about whether currency intervention will occur.

Market participants largely share the view.

Intervention is possible, but not guaranteed to occur immediately.

From 2024 to 2025, the government and BOJ conducted large-scale yen-buying interventions, briefly driving USD/JPY toward yen-strength. However, the effect did not last long.

The reason is simple: what the market cares about is the U.S.–Japan interest rate differential.

Interventions can temporarily change market sentiment but cannot alter the fundamental factors.

The Finance Ministry continues to say they will respond to excessive volatility, but this is effectively jawboning.

In actual intervention decisions, not only levels but speed matter. Being at 160 yen does not mean immediate intervention; a scenario where rapid rises occur in a short time would be more closely watched.

?What will happen with Governor Ueda’s hospitalization? Behind the Rate Hike Expectation

The big surprise this time was Governor Kazuo Ueda’s hospitalization.

From June 9, he was admitted for a liver cyst infection and is expected to be out for about two weeks.

Since the enactment of the new BOJ Act, it is the first time the Governor has missed a Policy Meeting.

Nevertheless, under BOJ rules, policy decisions can proceed without the Governor.

The Chair will be Vice Governor Shinzo Himi or Nomura Kounosuke? (翻訳上の表現) and press conferences are to be handled by Vice Governor Shinichi Uchida. Both the government and the BOJ say there is “no hindrance to policy operation.”

Nevertheless, because the timing was so impeccable, various rumors are circulating on social media.

Of course medical issues are the main cause. But the unusual situation of a Governor absent when rate hike expectations are rising has also, indeed, affected market sentiment to some extent.

?The Credibility of Rate Hikes and Market Pricing

So, will a rate hike really occur?

At present, the probability of an additional rate hike is high.

markets have priced in a lot already, and many economists also expect a rate hike.

Underlying factors are inflationary pressure from higher crude oil prices and wage increases from spring labor negotiations.

As companies pass on wage costs to prices, inflation is expected to continue rising.

On the other hand, current inflation is more cost-push driven by rising import costs, so there is debate about whether a rate hike is truly effective.

Because this is not demand-driven inflation, the yen’s appreciation may not be as large as the market hopes.

?The Takai Administration’s Shadow and the Delicate Balance with Public Opinion and the BOJ

The Takai Sanae administration fundamentally emphasizes growth.

From the standpoint of active fiscal policy and economic growth, they cannot help but be cautious about rate hikes.

Rate increases would raise mortgage burdens and increase corporate financing costs.

Meanwhile, dissatisfaction with inflation driven by a weaker yen is increasing.

If rates rise, concerns about the economy would grow; if they do not, criticism of high prices would intensify—a difficult situation.

The BOJ is an independent institution, but in reality it cannot completely ignore politics.

Therefore, the market watches not only monetary policy but political messaging as well.

?Rate hike decision vs. delay! What about the risk of a 165 yen move?

The market has already priced in a rate hike quite a bit.

Thus, even if a hike occurs, the USD/JPY may only strengthen by about 1–2 yen.

If the press conference is dovish, there could be a reversion to yen weakness as the “shock is over.”

On the other hand, if a rate hike is postponed, market impact could be large.

Since many market participants are assuming a hike, a postponement could accelerate yen selling.

A move toward 162, 163, or even 165 yen is quite possible.

If 165 yen is in sight, intervention vigilance would rise sharply.

Ultimately, the biggest factors moving the USD/JPY are the U.S.–Japan interest rate differential and energy prices.

A rate hike alone will not by itself eliminate the yen’s weakness.

?The BoJ Meeting is the Main Focus Going Forward

With the USD/JPY stabilizing in the 160s, expectations of BOJ rate hikes, Governor Ueda’s hospitalization, and distance from the Takai administration, June 2026’s forex market has many factors at play.

At present, a rate hike is the main scenario, but since the market has already priced in a lot, the yen’s strength effects are viewed as limited.

More importantly, the surprise would come from a delay in rate hikes.

In that case, a move toward 162–165 yen could accelerate the depreciation of the yen.

Also, currency intervention is only a time-buying measure; the fundamental issues are the U.S.–Japan interest rate differential and energy prices.

The main focus going forward is the BOJ meeting results announced on June 16 and the subsequent vice governor’s press conference.

Because markets can move significantly, both traders and households should assess the situation calmly.

Which do you expect more: rate hikes or keeping rates unchanged?

Practice and verify freely with a completely risk-free trade simulator!

Details page for One-Click FX Training MAX